Steep Drop In Refinance Activity Drives Continued Slump

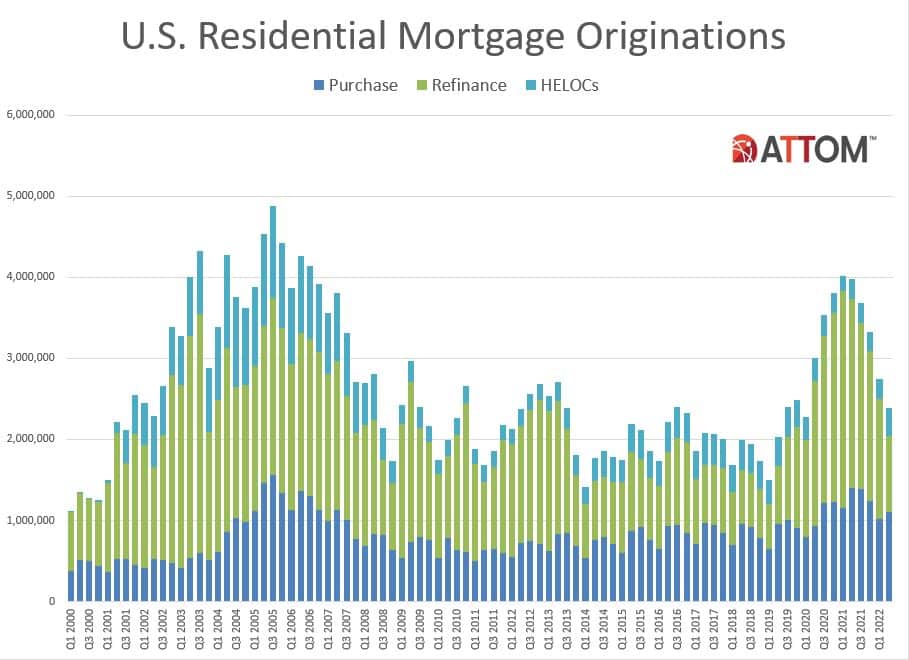

ATTOM released its second-quarter 2022 U.S. Residential Property Mortgage Origination Report, which shows that 2.39 million mortgages secured by residential property (1 to 4 units) were originated in the second quarter of 2022 in the United States. That figure was down 13 percent from the first quarter of 2022 – the fifth quarterly decrease in a row – and down 40 percent from the second quarter of 2021 – the biggest annual drop since 2014.

The decline resulted from another double-digit downturn in refinance activity that more than outweighed increases in home-purchase and home-equity lending.

Overall, lenders issued $807.8 billion worth of mortgages in the second quarter of 2022. That was down quarterly by 11 percent and annually by 35 percent. As with the number of loans, the annual decrease in the dollar volume of loans marked the largest in eight years.

“Mortgage rates that have virtually doubled over the past year have decimated the refinance market and are starting to take a toll on purchase lending as well,” said Rick Sharga, executive vice president of market intelligence at ATTOM. “The combination of much higher mortgage rates and rising home prices has made the notion of homebuying simply unaffordable for many prospective buyers, which threatens to drive loan volume down even further as we exit the spring and summer months.”

The downturn in total activity resulted from just 941,000 residential loans getting rolled over into new mortgages during the second quarter of 2022 – a figure that was down 36 percent from the first quarter of 2022 and down 60 percent from a year earlier. Amid another rise in mortgage interest rates, refinance lending decreased for the fifth straight quarter, hitting a point that was just one-third of what it was in early 2021. The dollar volume of refinance loans was down 35 percent from the prior quarter and 56 percent annually, to $310.1 billion.

For the first time since early 2019, refinance activity in the second quarter did not represent the largest chunk of mortgages, dropping to 39 percent of all loans. That was off from 53 percent in the first quarter and from a recent peak of 66 percent in early 2021.

Purchase-loan activity, meanwhile, increased modestly as the 2022 Spring home-buying season kicked into gear. Despite ongoing home-price spikes, the number of purchase loans rose 8 percent quarterly, to 1.1 million, representing 46 percent of all borrowing. Still, that gain was unusually small for the months running from April through June and left the number of purchase mortgages down 21 percent annually. The dollar volume of loans taken out to buy residential properties rose to $431.4 billion, up 15 percent from the first quarter of this year, but still down 12 percent from the second quarter of last year.

The best-performing category by far in the second quarter was again home-equity lending. Home Equity Lines of Credit shot up 35 percent quarterly and 44 percent annually, to 341,704.

“Borrowers looking to tap into their equity should know that HELOC activity has been particularly strong among credit unions and community banks, along with a small but growing number of depository banks,” Sharga noted. “While non-bank mortgage lenders may begin to more aggressively originate home equity loans, it’s not likely they’ll be active participants in the HELOC market.”

The latest loan trends reflected a housing market in flux, pushed by competing forces, and continued a sharp break from a period when lending activity nearly tripled from early 2019 through early 2021.

Total mortgages drop at fastest pace in eight years

Banks and other lenders issued 2,385,051 residential mortgages in the second quarter of 2022. That was down 13.2 percent from 2,747,324 in the first quarter of 2022 and down 40 percent from 3,976,656 in the second quarter of 2021. The annual decline marked the largest since the first quarter of 2014. The $807.8 billion dollar volume of loans in the second quarter was down 10.6 percent from $903.7 billion in the prior quarter and was 35 percent less than the $1.24 trillion lent in the second quarter of 2021.

Overall lending activity decreased from the first quarter to the second quarter of 2022 in 173, or 80 percent, of the 215 metropolitan statistical areas around the U.S. with a population of more than 200,000 and at least 1,000 total residential mortgages issued in the second quarter of 2022. Total lending activity was down at least 10 percent in 97 metros (45 percent). The largest quarterly decreases were in Knoxville, TN (down 59.9 percent); Roanoke, VA (down 52.7 percent); Charleston, SC (down 37 percent); St. Louis, MO (down 28.7 percent) and Philadelphia, PA (down 27.3 percent).

Aside from St. Louis and Philadelphia, metro areas with a population of least 1 million that had the biggest decreases in total loans from the first quarter to the second quarter of 2022 were New York, NY (down 25.9 percent); Detroit, MI (down 25.6 percent) and San Jose, CA (down 24.7 percent).

The biggest increases in the total number of mortgages from the first quarter to the second quarter of 2022 were in Atlantic City, NJ (up 32.5 percent); Erie, PA (up 18.8 percent); Peoria, IL (up 17.4 percent); Topeka, KS (up 15.6 percent) and Utica, NY (up 14.6 percent).

The only metro areas with a population of at least 1 million where total loan originations increased from the first to the second quarter were Honolulu, HI (up 9.9 percent); Kansas City, MO (up 3.4 percent) and Rochester, NY (up 3.2 percent).

Refinance mortgage originations slump to lowest point in three years

Lenders issued 941,111 residential refinance mortgages in the second quarter of 2022 – the smallest count since the second quarter of 2019.

The latest number was down 35.9 percent from 1,469,237 in first quarter of 2022 and 59.7 percent from 2,335,808 in the second quarter of 2021. The $310.1 billion dollar volume of refinance loans in the second quarter of 2022 was down 35.1 percent from $477.5 billion in the prior quarter and down 56.1 percent from $706.2 billion in the second quarter of 2021.

Refinancing activity decreased from the first quarter to the second quarter of 2022 in 213, or 99 percent, of the 215 metropolitan statistical areas around the country with enough data to analyze. Activity dropped quarterly by at least 25 percent in 162 metro areas (75 percent) and at least 35 percent in 94 metros (44 percent). The largest quarterly decreases were in Roanoke, VA (down 65.8 percent); Knoxville, TN (down 64.4 percent); San Jose, CA (down 58.5 percent); Oxnard, CA (down 56.3 percent) and Charleston, SC (down 55.3 percent).

Aside from San Jose, metro areas with a population of least 1 million that had the biggest decreases in refinance activity from the first quarter to the second quarter of this year were Portland, OR (down 53.2 percent); San Francisco, CA (down 52.9 percent); Sacramento, CA (down 51.8 percent) and Chicago, IL (down 49.8 percent).

The only metro areas where refinance lending increased from the first quarter to the second quarter were Atlantic, City, NJ (up 23.7 percent) and Utica, NY (up 8.5 percent).

Purchase mortgages increase in second quarter, but at relatively small pace

Lenders originated 1,102,236 purchase mortgages in the second quarter of 2022. That was up 7.6 percent from 1,024,109 in the first quarter. But the increase was the smallest second-quarter gain since at least 2000. As a result, purchase lending remained down 21.5 percent from 1,403,287 in the second quarter of 2021. The $431.4 billion dollar volume of purchase loans in the second quarter of 2022 was up 15.1 percent from $374.9 billion in the prior quarter, but down 11.8 percent from $489.2 billion a year earlier.

Residential purchase-mortgage originations increased from the first quarter of 2022 to the second quarter of 2022 in 173 of the 215 metro areas in the report (80 percent), but were still down annually in 194 metro areas (90 percent).

The largest quarterly increases were in Madison, WI (up 60.8 percent); Honolulu, HI (up 55.8 percent); Lafayette, IN (up 55.5 percent); Champaign, IL (up 52.6 percent) and Jackson, MS (up 49.3 percent).

Aside from Honolulu, metro areas with a population of at least 1 million that saw the biggest quarterly increases in purchase originations in the second quarter of 2022 were Boston, MA (up 41.7 percent); Seattle, WA (up 33.6 percent); Richmond, VA (up 31.9 percent) and Birmingham, AL (up 29.9 percent).

Residential purchase-mortgage lending decreased most from the first quarter to the second quarter of 2022 in Knoxville, TN (down 52 percent); Roanoke, VA (down 37.3 percent); Salinas, CA (down 18.1 percent); Ogden, UT (down 16.9 percent) and Boise, ID (down 13.6 percent).

Metro areas with a population of at least 1 million where purchase originations decreased most from the first to the second quarter of 2022 were New York, NY (down 12 percent); Los Angeles, CA (down 11 percent); St. Louis, MO (down 10.7 percent); Philadelphia, PA (down 10.7 percent) and Detroit, MI (down 9.5 percent).

HELOC lending up another 35 percent

A total of 341,704 home-equity lines of credit (HELOCs) were originated on residential properties in the second quarter of 2022, up 34.5 percent from 253,978 during the prior quarter and up 43.8 percent from 237,561 in the second quarter of 2021. HELOC activity increased for the fourth time in five quarters after decreasing in each of the prior six quarters. The $66.3 billion second-quarter 2022 volume of HELOC loans was up 29.4 percent from $51.2 billion in the first quarter of 2022 and 39.8 percent from $47.4 billion in the second quarter of last year, hitting the highest point in almost three years.

HELOCs comprised 14.3 percent of all second-quarter 2022 loans, more than double the 6 percent level from a year earlier.

HELOC mortgage originations increased from the first quarter to the second quarter of 2022 in 94 percent of the metro areas analyzed. The largest increases in metro areas with a population of at least 1 million were in Fresno, CA (up 82.9 percent); Riverside, CA (up 80.9 percent); Buffalo, NY (up 53.2 percent); San Diego, CA (up 52 percent) and Los Angeles, CA (up 51.5 percent).

The only quarterly decrease in HELOCs among metro areas with a population of at least 1 million was in St. Louis, MO (down 11.7 percent).

FHA loan portion continues to increase while VA share declines

Mortgages backed by the Federal Housing Administration (FHA) rose as a portion of all lending for the third straight quarter, accounting for 255,544, or 10.7 percent, of all residential property loans originated in the second quarter of 2022. That was up from 10.4 percent in the first quarter of 2022 and 9.6 percent in the second quarter of 2021.

Residential loans backed by the U.S. Department of Veterans Affairs (VA) accounted for 122,483, or 5.1 percent, of all residential property loans originated in the second quarter of 2022, down from 5.6 percent in the previous quarter and 6.8 percent a year earlier. VA lending as a portion of all loans dropped for the seventh straight quarter.

Down payments increase

The national median down payment on homes purchased with financing increased during the second quarter of 2022 after declining in the prior two quarters, while the typical amount borrowed rose to another new high. At the same time, the ratio of median down payments to home prices went up.

The median down payment on single-family homes and condos purchased with financing in the second quarter of 2022 increased to $35,000, up 34.7 percent from $25,980 in the previous quarter and up 34.6 percent from $26,000 in the second quarter of 2021. Among homes purchased with financing in the second quarter of 2022, the median loan amount was $320,000. That was up 8.1 percent from the prior quarter and up 12.3 percent from the same period in 2021.

The typical down payment in the second quarter of this year represented 9.1 percent of the purchase price, up from 7.4 percent in the prior quarter and 7.5 percent a year earlier.

The Place for Lending Visionaries and Thought Leaders. We take you beyond the latest news and trends to help you grow your lending business.