Commercial And Multifamily Delinquency Rates Continue To Vary

Commercial and multifamily mortgage performance remains mixed, revealing the various impacts the COVID-19 pandemic has had on different types of commercial real estate, according to two reports released today by the Mortgage Bankers Association (MBA).

The summary of findings come from MBA’s November Commercial Real Estate Finance (CREF) Loan Performance Survey, and the latest quarterly Commercial/Multifamily Delinquency Report for the third quarter of 2020. The CREF Loan Performance Survey was developed to better understand the ways the pandemic is impacting commercial mortgage loan performance. MBA’s regular quarterly analysis of commercial/multifamily delinquency rates is based on third-party numbers covering each of the major capital sources.

“Commercial and multifamily mortgage delinquency rates remain mixed, varying dramatically by property type, and therefore by capital source,” said Jamie Woodwell, MBA’s Vice President of Commercial Real Estate Research. “Much of the stress in the market is driven by loans, predominantly for lodging and retail properties, that became delinquent in April and May and have now transitioned to later-stage delinquencies. November did see small increases in newly delinquent retail, lodging and office loans, but at levels far below what was seen at the outset of the pandemic.”

Added Woodwell, “Different capital sources calculate delinquency rates in different ways, and those differences can cloud comparisons. Looking to 2021, widespread vaccinations should help the economy and commercial real estate – especially the hard-hit retail and leisure and hospitality sectors – start to recover at a faster pace by mid-summer. Between now and then, much will depend on how long the current surge lasts, and the degree to which it holds back economic activity.”

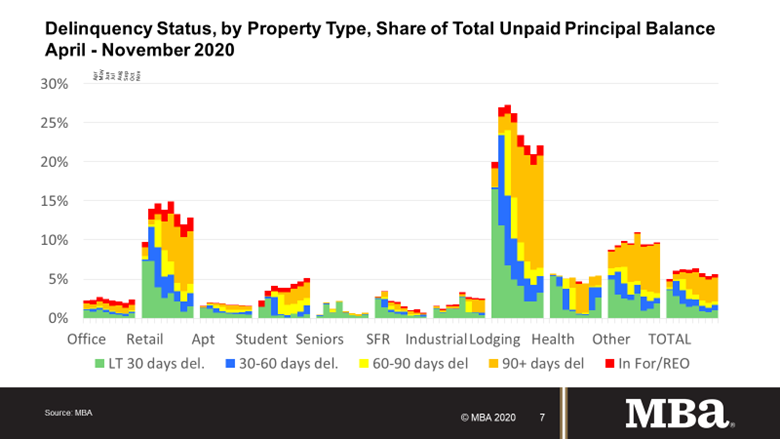

Key Findings from MBA’s CREF Loan Performance Survey for November 2020:

Note: The survey includes a range of delinquency measures, but for the purposes of understanding the impacts from the pandemic, any non-current loan is generally treated as delinquent.

The balance of commercial and multifamily mortgages that are not current increased for the first time in three months in November, driven by more loans becoming newly delinquent.

- 94.3% of outstanding loan balances were current, down from 94.6% in October.

- 3.5% were 90+ days delinquent or in REO, unchanged from a month earlier.

- 0.4% were 60-90 days delinquent, down from 0.6%.

- 0.7% were 30-60 days delinquent, up from 0.6%.

- 1.0% were less than 30 days delinquent, up from 0.7%.

Loans backed by lodging and retail properties continue to see the greatest stress, with a higher share of non-current loan balances entering late-stage delinquency. The overall share of lodging and retail loan balances that are delinquent increased in November, with an uptick in newly delinquent balances.

- 22.1% of the balance of lodging loans and 12.9% of the balance of retail loans were non-current in November, up from 21.0% and 12.0%, respectively, in October.

- Non-current rates for other property types were more mixed.

- 2.5% of the balances of industrial property loans were non-current, down from 2.6% in October.

- 2.4% of the balances of office property loans were non-current, up from 2.0% last month.

- 1.6% of multifamily balances were non-current, unchanged from a month earlier.

Because of the concentration of hotel and retail loans, CMBS loan delinquency rates are higher than other capital sources.

- 10.4% of CMBS loan balances were non-current in November, up from 9.9% in October.

- Non-current rates for other capital sources were more moderate.

- 2.8% of FHA multifamily and health care loan balances were non-current, up from 2.4% in October.

- 1.7% of life company loan balances were non-current, down from 1.8% in October.

- 1.3% of GSE loan balances were non-current, flat from October.

Key Findings from MBA’s Third Quarter of 2020 Commercial/Multifamily Delinquency Report:

Note: MBA’s quarterly report relies on the headline delinquency measures used by each capital source. Each capital source’s measure is different. The different measures can give a good indication of delinquency trends within a source, but should not be used to compare any one capital source to another.

- Commercial and multifamily mortgage delinquency rates increased for every major capital source in the third quarter of 2020, but the increases varied dramatically.

- Headline delinquency rates (30+ days delinquent or in foreclosure or REO) for the commercial mortgage-backed securities (CMBS) market decreased to 7.9%, which is down from the record of 9.6% in the second quarter of 2020.

- The 60+ day delinquency rate for life insurance company loans rose from 0.15% to 0.17% – roughly half the peak levels seen during the Great Financial Crisis and the recession in 2001.

- Fannie Mae reported a multifamily 60+ day delinquency rate of 1.12%, and Freddie Mac reported a rate of 0.13%.

- Note: Fannie Mae reports loans that are receiving payment forbearance as delinquent, while Freddie Mac excludes those loans.

- The 90+ day delinquency rate for commercial and multifamily loans held on bank balance sheets rose from 0.64% to 0.72%.

- MBA’s analysis incorporates the measures used by each individual investor group to track the performance of their loans. Because each investor group tracks delinquencies in its own way, delinquency rates are not comparable from one group to another.

The Place for Lending Visionaries and Thought Leaders. We take you beyond the latest news and trends to help you grow your lending business.