IMBs Report Pre-Tax Net Production Losses In Q1 Of 2023

Independent mortgage banks (IMBs) and mortgage subsidiaries of chartered banks reported a net loss of $1,972 on each loan they originated in the first quarter of 2023, an improvement from the reported loss of $2,812 per loan in the fourth quarter of 2022, according to the Mortgage Bankers Association’s (MBA) newly released Quarterly Mortgage Bankers Performance Report.

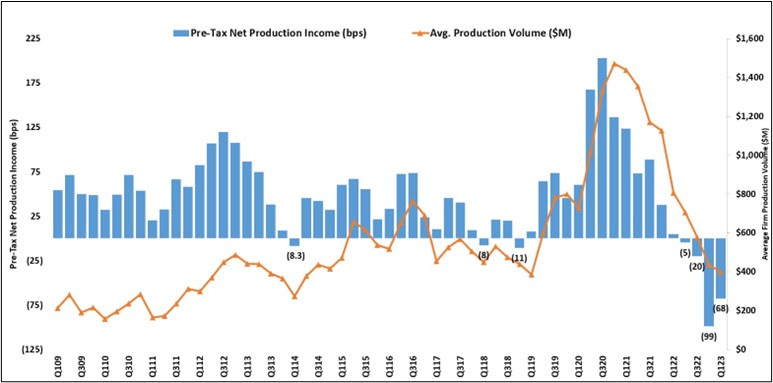

“A net production loss of 68 basis points in the first quarter of the year is an improvement over the record 99-basis-point loss reported in the fourth quarter of 2022,” said Marina Walsh, CMB, MBA’s Vice President of Industry Analysis. “Conditions continue to be challenging for the industry, with now four consecutive quarters of production losses and nine consecutive quarters of volume declines.”

Added Walsh, “One silver lining from the first quarter is that production revenues improved by 40 basis points. However, costs continued to escalate with the further drop in volume and reached more than $13,000 per loan despite substantial personnel reductions.”

In terms of profitability, Walsh noted that including both the production and servicing business lines, 32 percent of companies were profitable last quarter, up from 25 percent in the last quarter of 2022.

Key findings of MBA’s First-Quarter 2023 Quarterly Mortgage Bankers Performance Report include:

- The average pre-tax production loss was 68 basis points (bps) in the first quarter of 2023, compared to an average net production loss of 99 bps in the fourth quarter of 2022, and down from a gain of 5 basis points one year ago. The average quarterly pre-tax production profit, from the third quarter of 2008 to the most recent quarter, is 48 basis points.

- The average production volume was $398 million per company in the first quarter, down from $436 million per company in the fourth quarter. The volume by count per company averaged 1,264 loans in the first quarter, down from 1,395 loans in the fourth quarter.

- Total production revenue (fee income, net secondary marketing income and warehouse spread) increased to 358 bps in the first quarter, up from 317 bps in the fourth quarter. On a per-loan basis, production revenues increased to $11,199 per loan in the first quarter, up from $9,637 per loan in the fourth quarter.

- The purchase share of total originations, by dollar volume, remained unchanged at a study high of 88 percent in the first quarter. For the mortgage industry as a whole, MBA estimates the purchase share was at 80 percent in the first quarter of 2023.

- The average loan balance for first mortgages increased to $329,159 in the first quarter, up from $322,225 in the fourth quarter.

- Total loan production expenses – commissions, compensation, occupancy, equipment, and other production expenses and corporate allocations – increased to a study-high of $13,171 per loan in the first quarter, up from $12,450 per loan in the fourth quarter of 2022. From the third quarter of 2008 to last quarter, loan production expenses have averaged $7,172 per loan.

- The average number of production employees per company declined from 413 production employees in the fourth quarter of 2022 to 374 production employees in the first quarter of 2023 (on a repeater company basis).

- Servicing net financial income for the first quarter (without annualizing) was $54 per loan, up from $37 per loan in the fourth quarter. Servicing operating income, which excludes MSR amortization, gains/loss in the valuation of servicing rights net of hedging gains/losses, and gains/losses on the bulk sale of MSRs, was $102 per loan in the first quarter, down slightly from $104 per loan in the fourth quarter.

- Including all business lines (both production and servicing), 32 percent of the firms in the study posted pre-tax net financial profits in the first quarter, up from 25 percent in the fourth quarter.

The Place for Lending Visionaries and Thought Leaders. We take you beyond the latest news and trends to help you grow your lending business.