iEmergent Forecasts A Slightly Better Housing Market

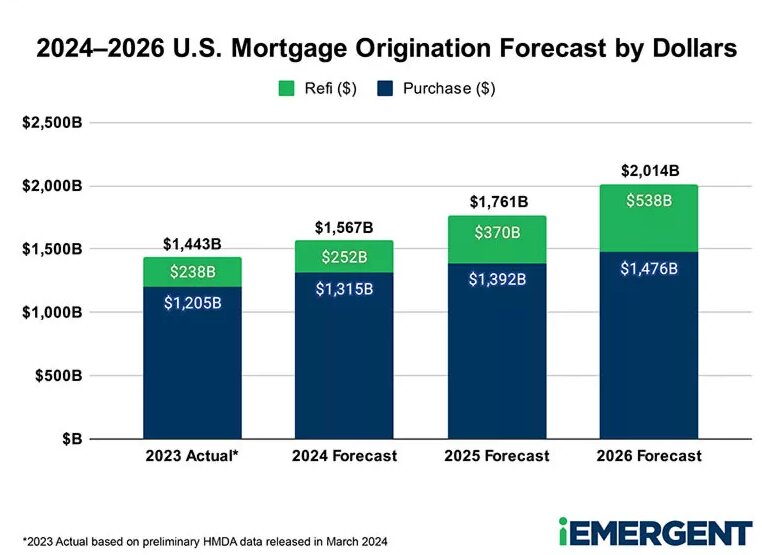

At the end of March, the preliminary HMDA data for 2023 was released, so iEmergent has updated its mortgage origination forecast to align with that new information. For 2023, first lien mortgage originations totaled $1.44 trillion, a 37% decline from 2022 and the lowest level since 2014. Moreover, the company expects this year will only be slightly better. The forecast for 2024 is $1.59 trillion, with only a modest increase in purchase volume – mostly driven by loan size increases – and continued low levels of refinances.

According to iEmergent Chief of Forecasting Mark Watson, persistent economic trends – including inflation, real GDP growth, a strong labor market and tight Federal Reserve monetary policy – will continue to dampen the mortgage origination market for the next three years:

- 2024: Although purchase dollar volume is expected to increase by about 9% in 2024, most of the volume gain will be attributable to larger average loan sizes rather than significant growth in loan count. Refinances are forecast to reach 18% of total mortgage originations, only slightly more than their record low of 17% in 2023.

- 2025: By 2025, deceleration and, ultimately, a mild decline in GDP growth should help reduce long-term interest rates and soften home prices, leading to slightly higher mortgage origination levels. Refi units are anticipated to grow 33% (albeit from historically low levels) on a year-over-year basis.

- 2026: By 2026, total U.S. mortgage origination volume is expected to exceed the $2 trillion mark for the first time since 2022 as refinances continue to recover share in both loan units and dollars.

The strength of the overall American economy continues to surprise on the upside. That strength has resulted in a slower-than-expected decline in long-term interest rates which has hobbled both purchase and refinance origination prospects. In fact, recent months’ data on the strong labor market and disappointing news on disinflation resulted in rising short- and long-term interest rates in the first four months of the year before declines occurred in the latest month.

The major macroeconomic indicators still look generally positive, but chronic problems in the housing market will dampen the mortgage origination outlook:

- Inflation: The Fed’s preferred inflation indicator, the change in the core PCE price index (personal consumption expenditures price index excluding food and energy), has fallen steadily. In 17 of the 18 months since September 2022, the year-over-year change has declined, reaching 2.8% in March – not quite down to the Fed’s 2% target but moving in the right direction.

- Real GDP: Since its slight hiccup in early 2022, real GDP growth has been strong, with the latest year-over-year growth rate at a robust 3.0% in Q1/2024 – an unexpected and remarkable feat in the current tight monetary policy environment.

- Employment: The labor market also continues to be unexpectedly strong. With the rapid rise in interest rates, most economists had projected at least a percentage point rise in the unemployment rate last year. Despite that pessimism, it hardly moved and is still under 4%, not much higher than what it was before COVID hit (3.5%) – which was the lowest since the 1960s.

- Interest rates: On the short-term side, the Federal Reserve hasn’t raised the Fed Funds target rate since its last hike to 5.25-5.50% in July last year, but it is maintaining its tight monetary policy stance. While Fed Chair Powell said early in the year we were “not far” from where the Fed might begin cutting rates, it doesn’t appear now that that will happen until late summer at best. On the long-term side, the 10-year Treasury yield is bouncing around between 4.0-4.5%, while the 30-year fixed mortgage rate is bouncing around 7.0%.

However, the housing market is a challenge. On the one hand, rising home price pressure indicates housing demand remains strong. On the other hand, depressed home sales levels suggest weakening demand. Total home sales (existing home sales plus new single-family homes) were 4.767 million in 2023, 22% lower than the pre-pandemic 2019 level of over 6 million. Adjusting for the growth in the number of households in that time, current home sales are nearly 25% below that 2019 level.

It might seem like inconsistent signals, but it’s not. The housing market is severely depressed due to chronic inventory shortage, a constant condition over the last decade that’s only gotten worse in the last few years. Low supply creates rising pressure on prices. Prices have gotten high enough that they are unaffordable for many potential homebuyers, hence the depression in sales. Yet home prices will continue to have upward pressure because homebuyers remaining in the market must bid them up to compete for the meager supply of homes available for purchase.

Unaffordability has become particularly acute in the last two years because rising interest rates have raised the cost of mortgage payments. But even before that, another, more fundamental force was also driving unaffordability. Since the pandemic, home prices have risen much faster than household incomes. In our estimation, the gap between home prices and household income has reached a similar magnitude as the one that triggered the housing bust of 2007 and led to the Great Recession.

iEmergent now believes that there will NOT be a recession this year, but that the U.S. economic juggernaut will continue to roll on into 2025, though at a decelerating pace. This will result in a slower decline in long-term interest rates than many economists expect, even if the Fed begins to cut short-term rates this year. As a result of high interest rates and the home price / income gap, the company expects home sales to continue at their current weak pace, eventually leading to softening home prices going into next year, though there’s some risk that sales levels may fall even lower.

For 2024, iEmergent forecasts a 9% increase in purchase dollar volume but only a 2.8% increase in loan counts, so most of the gain will be due to increases in average loan size. The company expects refinances to rise to only 18% of mortgage originations, only slightly more than their record low of 17% in 2023.

By 2025, iEmergent expects further deceleration in GDP growth and ultimately a mild decline. The resulting lower long-term interest rates and softening home prices should lead to slightly higher mortgage origination levels. Refinance volumes should increase significantly, albeit from historically low levels, but purchase volume growth may slow.

The Place for Lending Visionaries and Thought Leaders. We take you beyond the latest news and trends to help you grow your lending business.