Marketpulse: Black Knight Data Shows COVID-19 Unemployment Spike Triggering Challenges

The Data & Analytics division of Black Knight, Inc released its latest Mortgage Monitor Report, based upon the company’s industry-leading mortgage performance, housing and public records datasets. This month, in light of the growing impact of the COVID-19 pandemic on the economy, Black Knight drilled down into aspects of its extensive white paper exploring the ramifications of this crisis for the real estate and mortgage industries. As Black Knight Data & Analytics President Ben Graboske explained, any attempt to quantify potential delinquencies from the current situation is challenging, as there have been no true corollaries in history.

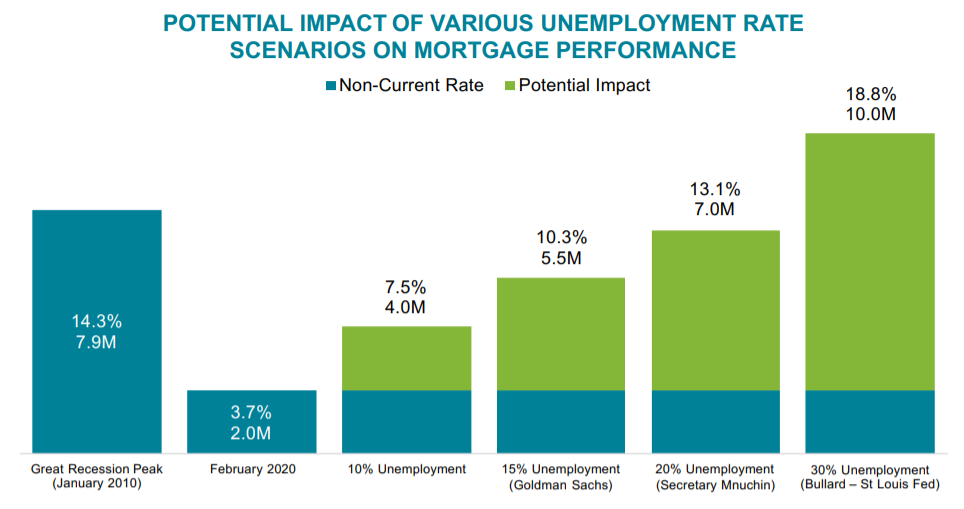

“Trying to gauge the impact of COVID-19 on mortgage performance is as much an art right now as a science,” said Graboske. “The fact is that there is no true point of comparison in the nation’s recent history for analysts to model against. That said, there are some historical clues that can help shed light. In the Great Recession, for example, the number of past- due mortgages tripled over four years, increasing by more than 5.5 million, as the unemployment rate rose relatively sharply from 4.5% in 2006 to 10% by the end of 2009. Today, we’ve seen more than 10 million people file for unemployment since the coronavirus was labeled a pandemic on March 11, which should put the unemployment rate at roughly 9.5%. Using the Great Recession as a point of comparison, Black Knight’s AFT modeling team looked at potential delinquencies under different unemployment scenarios, and at 10%, we could expect 2 million new mortgage delinquencies. That would put the total at 4 million delinquencies with a national non-current rate of 7.5%. If unemployment climbs to the 15% recently projected by Goldman Sachs, we could be looking at 5.5 million past-due mortgages. Should unemployment reach the 32% projected by the Federal Reserve Bank of St. Louis, the non-current rate could spike to nearly 19%, surpassing what we saw during the Great Recession, with 10 million homeowners past due on their mortgages.

“The various forbearance programs being offered to borrowers via the recently passed CARES Act, as well as via individual agencies and mortgage servicers, are a key difference today. Mortgage performance in the wake of natural disasters gives an idea of how well such programs have worked to help keep people in their homes. Pointing to the effectiveness of forbearance programs in a time of crisis, of the more than 140,000 seriously delinquent mortgages caused by the 2017 hurricane season, just 1% of homes were lost to foreclosure or short sale two years after the storms. Although, should financial disruptions become more long-term, additional assistance programs may become necessary. Of course, a surge of forbearance requests brings its own challenges, both operational and financial.

“Mortgage servicers are already being inundated with such requests, and those without the proper technology solutions or staffing levels in place will be hard-pressed to manage the situation. Likewise, servicers still need to pay principal and interest (P&I) advances to federally backed securities holders, even if borrowers are granted deferments on paying their mortgages. If even just 5% of homeowners with GSE- or GNMA-securitized mortgages seek forbearance, those costs would be more than $2.1 billion per month. At 10%, the monthly cost owed to securities holders would jump to $4.2 billion and at 20% to $8.48 billion. While Ginnie Mae has announced a pass-through assistance program through which it will advance principal and interest payments to investors on behalf of servicers, at present there is no such program in place for mortgages backed by the GSEs. This remains a very fluid situation all around.”

The month’s report also looked at the impact recent interest rate volatility has had on everything from home affordability and refinance incentive to home purchasing power. Market uncertainty has resulted in the spread between 10-year Treasury yields and 30-year fixed interest mortgage rates expanding significantly in recent weeks. Historically, the two move in relative tandem, but surges in refinance applications, which have overwhelmed originator supply chains along with uncertainty in the secondary markets, have resulted in 30-year rate increases and widening spreads. Such interest rate volatility has had a whipsaw effect on refinance incentive, with the number of homeowners who could both likely qualify for and benefit from a refinance growing as high as 14.3 million at the start of March, to as low as 3.3 million by March 12 and back to 10 million as of March 24.

Purchase demand, which has been hampered by economic uncertainty and social distancing efforts in recent weeks, is also experiencing downward pressure from recent interest rate volatility. After seeing home affordability improve to its strongest level in more than three years, with 30-year rates falling below record lows in early March, recent jumps in 30-year rates have significantly shifted the affordability landscape, seemingly on a daily basis. The payment required to purchase the average-price home has fluctuated by more than 13% over the past two weeks, making it difficult for prospective buyers to gauge how much home they qualify to purchase and creating challenges for those under contract to decide when to lock in their rate. For example, the buying power of a prospective homebuyer who qualified for a $1,000/month mortgage payment with 20% down rose from $270,000 at the start of the year to $292,000 on March 2 – when 30-year rates fell to 3.13%. When rates hit 4.15% two weeks later, that same borrower would have only qualified for a $258,000 home purchase – a $34,000 reduction in buying power.

The Place for Lending Visionaries and Thought Leaders. We take you beyond the latest news and trends to help you grow your lending business.