New Data Emerges On The COVID Housing Boom

New insights from iEmergent report that the COVID housing boom of 2020-2021 was characterized by very strong demand and limited housing supply. Not surprisingly, those conditions resulted in rapid home price acceleration. Young potential homebuyers — primarily from the Millennial generation and those saddled with student debt levels unmatched by previous generations — were certainly challenged by the low-supply / rising-price environment. How did this group fare during this home sales boom?

When the COVID-19 pandemic hit in early 2020, the home sales market briefly cratered along with the rest of the economy, but then it exploded as demand surged. Record low mortgage rates and a substantial fiscal stimulus sparked the surge, but sheltering in place and working from home also fueled a strong increase in the demand for homeownership. Home sales peaked in the second half of 2020, at their highest levels since 2006, and despite a dip following that peak, they maintained high levels throughout 2021. In fact, though no month in 2021 had higher levels than those from the peak of 2020, the aggregate sales volume in 2021 exceeded the volume in 2020, mostly due to the very low levels in the first couple months of the pandemic.

Home prices also soared during the COVID boom. They had been gradually increasing at an average annual rate of 4.8% from 2014 through 2019, but with the added demand ignited during the sales boom, the annual price increase quadrupled to more than 19.3% from mid-2020 through early 2022, according to the Case-Shiller Home Price Index.

Some homes are purchased in all-cash deals, but most are financed with mortgage loans. For the last several years, the Home Mortgage Disclosure Act (HMDA) data has captured the purchaser’s age on mortgage loan applications and fundings, and they have reported that information in fixed age-group segments.

With fixed age-group segments, the composition of households falling into each age-group bucket by generation changes from one year to the next. Back in 2018, people from the Millennial generation were from 22 to 37 years old, according to Pew Research. Thus, virtually all the homebuyers from the Under-25 segment were probably Millennials (since not many people under 22 can buy a house). However, in 2022, Millennials were 26 to 41 years old. By that time, the under-25 homebuyers were, by definition, all from Gen Z, the generation after the Millennials.

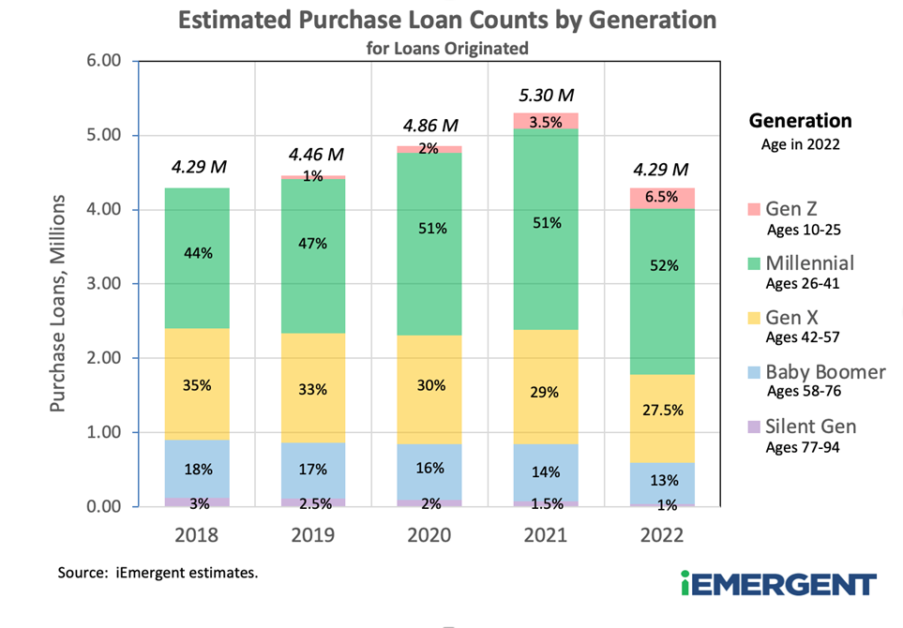

For most of the 2018-2022 period, the 25-34 segment has been composed entirely of Millennials, but during this period, more of the older Millennials have shifted into the 35-44 segment. By 2022, Millennials were the dominant generation in both the 25-34 segment and the 35-44 segment. Based partially on a Corelogic analysis of the mortgage market and partially on iEmergent’s own calculations, we have estimated how the last few years of originations have broken down by generation.

Our first observation concerns the magnitudes of the boom and bust. Purchase mortgage loan counts increased by 3.9% in 2019 (a “normal” purchase count gain), but then increased by 9.0% in 2020 (the first year of the pandemic boom), and another 9.1% in 2021, before falling -19.3% in 2022. This is similar to other boom-bust patterns the purchase market has experienced before.

Second, the segment of households from 25-34 years old continues to be the biggest in purchase mortgages, with the 35-44 segment always the second biggest. Although each of these age group segments comprised less than one third of purchase originations, the Millennial generation, which overlapped them, accounted for over half of purchases in 2022. In fact, Millennials have had over half of home purchases for the last three years (2020-2022). Even in the 2018-2019 period, they had a plurality of loans originated — more loans than any other generational segment.

Third, during 2020, the two youngest segments — the Under-25 and the 25-34 segments — increased their share of home purchase mortgages, decreasing share by the older homebuying segments. Those younger segments grew faster than the older segments and thus became larger shares of the whole. The combined purchases from those two younger segments grew more than 15% in 2020, while the combined purchases from the remaining five segments only grew 5%. It was the surge from the younger segments that initiated the boom.

Fourth, during 2021, the two youngest segments snapped back to their normal (pre-2020) share, while the 35-44 segment picked up the share the younger segments gave up.

Fifth, the share of homebuyers above age 55 decreased over the entire 2018-2022 period. (Note: While COVID mortality disproportionally affected the elderly, we don’t think it had much of an impact on purchase dynamics for households in the older segments. For one thing, the biggest impact from COVID mortality occurred in 2020, but then was reduced sharply in 2021 and 2022 as vaccines were widely released. Yet the older by-age segments still show declines in those latter years.)

Although the changes in purchase mortgage share over this period were small, they lead us to conclude that:

(1) Despite their higher debt load, younger households, primarily from the Millennial generation, had no trouble keeping up in the low-supply / rising-prices environment of the COVID housing boom. In fact, during the boom, they drove a larger share of housing purchases than they did in the more normal years of 2018 and 2019.

(2) Moreover, during the first year of the boom, the younger households of the Millennial generation led the charge. Nearly all of them would have been first-time homebuyers (FTHBs), eager to move out of parents’ homes and rental units, a sentiment that increased with the low interest rates and bunker mentality brought on by the pandemic.

(3) However, by the second and final year of the boom, older Millennials from the 35-44 segment had the faster-growing influence on housing purchases. A growing share of these households were likely repeat homebuyers, though many of them would have been FTHBs as well. The repeat homebuyers would have been eager to move up to larger homes to accommodate their growing families. It had probably taken them longer to complete their housing transitions because they had to sell their first homes in addition to finding their new ones. Their transitions might also have been more complicated by the effects of school-age children.

(4) Older homeowners, primarily from the Baby Boomer generation who in 2022 were 58-76 years old, hunkered down during the sales boom of the first two years of the pandemic and even during the sales bust afterwards. They already had a shrinking share of home purchases before the pandemic, but during the boom and into the bust, the pace of the decrease grew. This exacerbated the already low supply of homes available for sale because older homeowners were giving up their existing homes at an increasingly slower rate.

In addition, with the record-low interest rates during the boom, most older homeowners refinanced and locked in rock-bottom mortgage rates. To the extent they need to get a mortgage for any future home purchases they make, their new interest rates will most likely be considerably higher than their current rates, so they will be less likely to make that move. This could continue to restrict the pool of existing homes available for sale for years to come, thus increasing upward pressure on home prices as well.

The last few years have been a pivotal period for home purchase dynamics, particularly for younger homebuyers, but also for older homebuyers as well. Our analysis has shown the impact of the COVID pandemic and accompanying economic stimulus (primarily record-low interest rates) on homebuying across age groups. Young homebuyers, primarily from the Millennial generation, were the main drivers of the COVID home sales boom of 2020-2021, despite their higher educational debt burdens. Our analysis has also chronicled the emergence of Generation Z into the homebuying market and given us an early look at their growing impact on that market.

For older homebuyers, their waning impact on the purchase market has accelerated. Furthermore, older homeowners who refinanced during the low-rate period of 2020-2021 will likely contribute to a worsening supply squeeze of existing homes available for sale that will create upward pressure on home price appreciation for years.

Analyzing the mortgage market with a source as comprehensive and rich in detail as the HMDA data enables us to quantify trends in the housing market and better understand the mortgage customer.

The Place for Lending Visionaries and Thought Leaders. We take you beyond the latest news and trends to help you grow your lending business.