Marketpulse: Optimal Blue Sees The Impact Of Rate Movement And Loan Characteristics On Servicing Value

In terms of the secondary market, a mortgage loan is essentially made up of two separate parts, the loan asset and the servicing asset – which may be split up, packaged, and sold separately. The largest of the two pieces is the loan asset, which is cashflow of the loan itself, including most of the interest paid. The smaller piece is the servicing asset, which is part of the interest rate that is separated out in order to pay the servicer that acts as the monthly payment collector. The servicing asset, or servicing “strip”, is usually 0.25% on conventional loans and 0.19% to 0.565% on GNMA loans. There is an entire industry built around the servicing strip, which lenders can choose to sell or retain.

Servicing is valued by examining the present value of the cashflows associated with the servicing strip and adjusting those by the probabilities of prepayment and/or delinquency/default. This combination of simple financial accounting with relatively complex probability modeling, forecasts, and simulations, allows for a reliable valuation of very uncertain assets. This value moves with changes to the underlying assets, such as partial prepayments or delinquencies, as well as changes in the market.

The two primary risks to the servicing asset are prepayment risk and default risk. Prepayment risk is the risk that the loan pays off sooner than initially expected. Default risk is the possibility that the loan stops paying for some other reason. In general, prepayment risk dominates, being substantially more pervasive than default risk. However, default risk also presents substantial costs to the servicer (collections, advances, recovery, foreclosure, liquidation, etc.). Further, the magnitude of these risks fluctuates by credit worthiness. For instance, borrowers with good credit are even more likely to prepay (refinance or purchase another property), while those with poor credit are more likely to default as refinancing or purchasing another home may not be realistic possibilities.

In our current rate environment, the borrower on a loan originated only one year ago, will, in many cases, see substantial savings when refinancing at today’s rates. If the borrower does opt for a new loan, you also want to know the probability of recapture[1]. Finally, it is important to recognize the costs associated with servicing delinquent loans, such as advances, increased collections, foreclosure/legal fees, etc. These factors can have a substantial impact on the profitability of servicers.

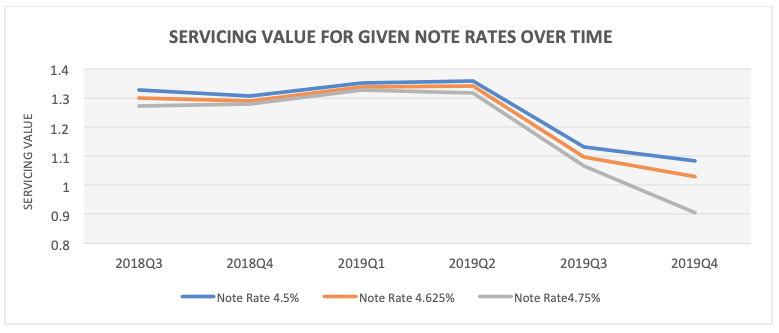

Below, we show how values changed over the last six quarters by note rate, holding other factors fixed.

Bear in mind that rates plummeted in the second half of 2019. Low note rate loans (e.g. 4.5%) have higher and more stable value because the prepayment risk is mitigated. However, borrowers paying higher note rates (e.g. 4.75%) are more likely to be “in the money” for a rate/term refinance, substantially increasing prepayment risk. The servicing strip is a significant piece of the loan and its profitability, but all of this is often an afterthought. Careful consideration is necessary to avoid losing a lot of money if retaining servicing or buying servicing rights. However, there can be substantial profit in retaining servicing whether it will be serviced in-house or a sub-servicer is utilized.

Having a strong servicing business connected to your origination channel can help steady the ship when the economy dips and origination volume dries up.

[1] How likely the owner of the servicing asset is to originate a refinance or new purchase loans from the borrower.

Tony Garritano is the founder at PROGRESS in Lending Association. As a speaker Tony has worked hard to inform executives about how technology should be a tool used to further business objectives. For over 20 years he has worked as a journalist, researcher and speaker in the mortgage technology space. Starting PROGRESS in Lending Association was the next step for someone like Tony, who has dedicated his entire career to providing mortgage executives with the information that they need to make informed technology decisions to help their businesses succeed.